Take 5 to Focus on 5

Discover five property examples that investment property owners need to be aware of for insurance purposes.

Learn why investment property owners should inventory their property.

It is important for all investment property owners to inventory exactly what makes up their investment property. For insurance purposes, it is worth the owner’s time and effort to do a mental and physical walkthrough with pen and paper (or computer) and document exactly what is considered part of your investment property.

The following are simplified examples for illustrative purposes only. Bear in mind that actual policy terms, conditions, limits, and deductibles always apply.

- In addition to the primary structure, what outbuildings are located on the property, i.e. sheds, storage units, garages? Investment properties that are one-to-four-family dwellings may be written on the Dwelling Property Form or the Commercial Property Form. The Dwelling Property Form covers “other structures up to 10% of dwelling” located at the described policy location, while the Commercial Property Form does not.

Larger investment properties, such as apartment complexes, must be written on the Commercial Property Form, which does not extend coverage to outbuildings. Under the Commercial Property Form, each structure must be separately scheduled with a separate limit, subject to additional premium.

- What type of tools and equipment do you own and keep at your investment property location? Standard property insurance provides coverage for small tools, equipment owned and used by the investment property owner for the purpose of maintaining and repairing the investment property. These items need to be kept on the investment property premises. Any expensive equipment items owned by the investment property owner that are located on the insured premises and used to maintain the building or its premises, such as lawnmowers, appliances, or tools, could or may need to be separately scheduled and are subject to an additional premium. The premium depends on the values, and a lower deductible may apply to contents and scheduled items.

- Does your investment property have underground wires, pipes, or tanks? Depending on the insurance company, property coverage may be available through endorsement for an additional charge.

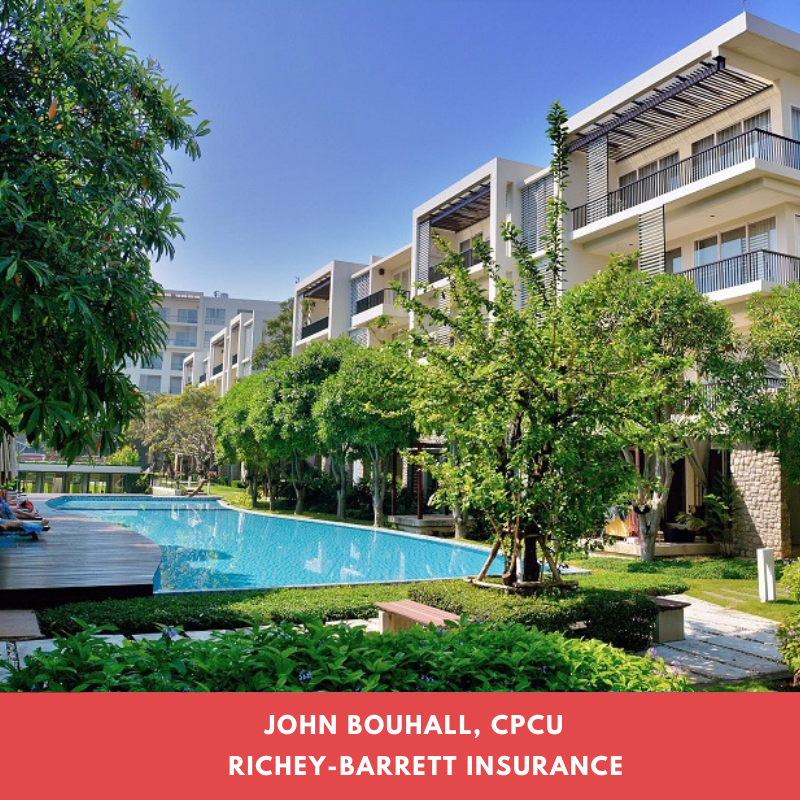

- Does your investment property include a pool? Pools maybe covered as part of the building or as additional location on premises covered under the Commercial Property Form.

Respects the Dwelling Property Form, in-ground pools are considered “other structures”. For above-ground pools, depending on the size and assembly/disassembly, they may or may not be “other structures”. Above-ground pools are more susceptible to damage from wind, hail, and falling debris.

Regardless of:

a. what type of pool exists, or

b. what policy form applies (Dwelling Property Form or Commercial Property Form)

be sure to advise your independent insurance agent before a loss or claim occurs. If your investment property has a pool, it is likely you will need to schedule it separately for an additional premium charge.

- Does your investment property include fencing? Fencing is specifically excluded under the Commercial Property Form. Under the Dwelling Property Form, fencing is considered an “other structure”. If your investment property has fencing, discuss this issue with your independent insurance agent. Depending on the quality and extent of your fencing, you may consider scheduling the fencing itself, subject to additional premium.

The above examples should help investment property owners organize what they own and what amount of property insurance coverage they need to consider beyond basic property coverage.

Richey-Barrett Insurance is your Trusted Choice Independent Insurance Agent for investment property insurance. We are available to discuss your unique insurance needs and provide you with competitive quotes for quality Property insurance, General Liability insurance, and Umbrella Liability insurance.