It’s Weather, Not Whether

Read current trends related to windstorm/hail in the Ohio homeowner’s insurance market.

Learn why and how windstorms and hail affect homeowner’s insurance coverage in Ohio.

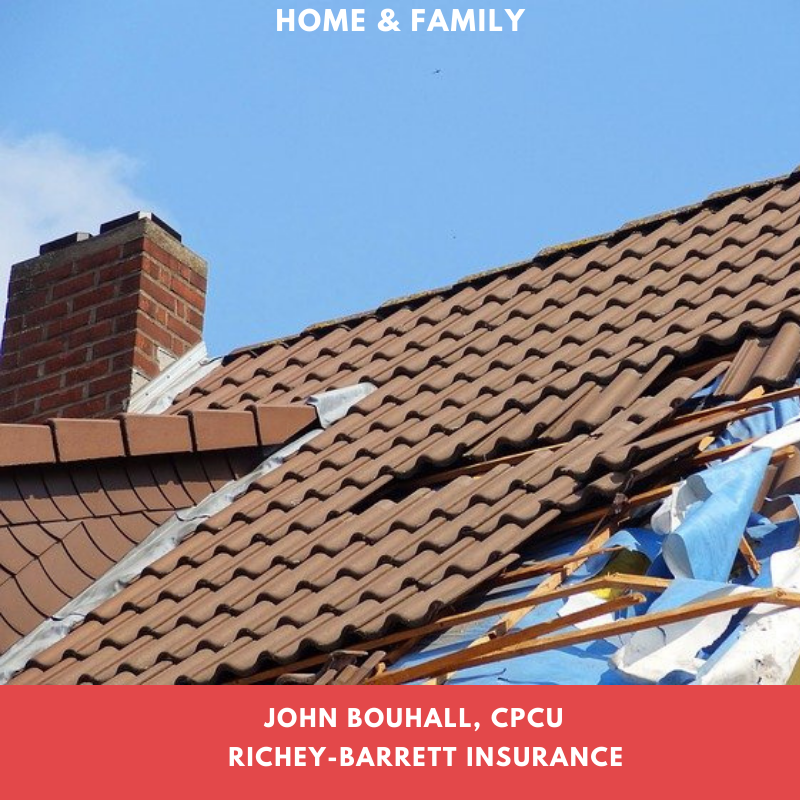

In Ohio, windstorm or hail is an insured peril under the standard homeowner’s insurance policy. Importantly, Ohio is one of several states in which these two weather events are on the radar. It’s not whether windstorms or hail will occur; it’s how often and how severe the weather is, which in turn directly impacts homeowner’s insurance coverage.

It used to be that a standard homeowner’s insurance policy in Ohio covered damage due to windstorms or hail on a replacement cost basis less regular deductible. This is changing, and changing quickly, due to three main, current, and foreseeable factors:

1. Increasing frequency and severity of weather patterns

2. Larger and higher-value homes

3. Rising costs of repair

These three factors are driving a trend in which some homeowner’s insurance companies are transferring part of the loss due to windstorms or hail to you, the homeowner. Buyer beware. Coverage terms relating to the windstorm or hail peril in the standard homeowner’s insurance policy has been or is being modified by some companies. You need to get the facts and understand what you are buying.

Below are four general examples* of trends we’ve seen in the Ohio homeowner’s insurance market, since at least 2015. Windstorm or hail is the insured peril in each example. EXAMPLE #1 and EXAMPLE #2 depict straightforward modifications of the wind/hail per claim deductible. EXAMPLE #3 and EXAMPLE #4 involve changes in how much of a wind/hail damage claim is actually paid by a homeowner’s insurance policy.

EXAMPLE #1:

Flat deductible per wind/hail claim. Typically, we are seeing a flat wind/hail deductible that is double the regular deductible.

– If your homeowner’s insurance deductible is $500., your wind/hail per claim deductible would be $1,000.

EXAMPLE #2:

Wind/hail per claim deductible based on the percentage of the insured value of the home. The usual range in Ohio is between ½% to as much as 2%. We rarely see anything higher than 2%.

– If your home’s insured value is $200,000.,:

a. a ½% deductible would be $1,000.00 per wind/hail claim.

b. a 1% deductible would be $2,000.00 per wind/hail claim.

c. a 2% deductible would be $4,000.00 per wind/hail claim.

EXAMPLE #3:

Maximum amount paid by homeowner’s insurance policy for a wind/hail claim based on a percentage cap of the home’s insured value.

– A 5% cap on a home with an insured value of $200,000. means the homeowner’s insurance policy would pay a maximum amount of $10,000.00. From a practical standpoint, realize the replacement cost to a full roof due to wind/hail damage in Ohio would easily exceed $10,000.; a homeowner’s policy with this modification would leave the insured homeowner out thousands of dollars.

EXAMPLE #4:

With respect to windstorms or hail damage to a roof that is older than 15 to 20 years, some homeowner’s insurance companies have modified their policies from replacement cost settlement to actual cash value settlement. The difference in loss payment between the two is significant. Even using a low depreciation rate of 30%, the loss payment difference could be $6,000. on a $20,000. wind/hail roof claim. That’s a lot of money to come up with quickly to put a roof over your head.

*The examples are for illustrative purposes only. Actual policy terms, conditions, and limits apply.

While most of these modifications are stated on the homeowner’s policy declarations page, many insureds do not understand the practical effect of the modifications until they have a wind/hail claim.

Call your Trusted Choice Independent Insurance Agent at Richey-Barrett Insurance for a no-obligation review of your homeowner’s insurance policy. We’ll help you weather through the trends and do our best to provide you with quality homeowner’s insurance.